Norway possesses the largest petroleum reserves in Western Europe and is a leading Oil&Gas

producer in the European region. The petroleum sector in Norway had been a crucial

contributor in the country’s economy, with approximately 20% share in the GDP and accounts for

45% of export revenues in 2014. Norway’s entire Oil&Gas reserves are located in its offshore

region, which comprises mainly of Norwegian Continental Shelf (NCS). The NCS is divided into

three divisions; the North Sea, Norwegian Sea, and the Barents Sea, of which the North Sea area

yields bulk oil production. The major crude oil producing fields in 2014 were Troll and Ekofisk,

both located in North Sea area of NCS. Due to the dynamic upstream sector of Norway, a great

potential for petroleum exploration is there in the Barents Sea, which holds the majority of

undiscovered petroleum resources; which can definitely match the active North Sea area in

resource development. An important upstream player in Norway is a government-controlled

company; Statoil, which delivers approximately 70% of country’s Oil&Gas production, and is the

front-runner in attracting investments to Norway’s petroleum sector.

According to latest industry facts, Norway has approximately 8000 million barrels of crude oil as

proved reserves and clocked oil production of 1948 thousand barrels per day in 2015. In terms

of natural gas, it has 1.9 trillion cubic meters of proved gas reserves and 117.2 billion cubic

meters of natural gas production in 2015. Due to mature oil fields, the oil production had

reduced currently as compared to past years, and it also reflects the oil market down-slide in

last two years. Although overall investments in the upstream sector had declined in recent years

due to weak global oil markets, a meager 10% dip is noted in total investments inflow as of

August 2015 vis-a-vis previous year. The majority of investments had been diverted towards

operations shut down and plant facilities removal at old mature fields. Despite the decrease in

global oil consumption and weak industry sentiments along with pressure to cut carbon

emissions, the government has solid plans to move ahead with firm initiatives. In August 2015,

Norway progressed with the development plan of its Johan Sverdrup gas field in the North Sea to

instill fresh confidence in the global petroleum business investors’ community and

simultaneously boosting the sentiments of Norwegian Oil&Gas sector in wake of low oil prices

scenario. Johan Sverdrup Oil&Gas field is projected to start production by the end of 2019, with

expected oil production in the range of 315,000 to 380,000 barrels per day in its first project phase.

Initial investments in this field development project had been finalized in the range of NK

(Norwegian Krone) 117 billion to NK 120 billion. The Norwegian Petroleum Directorate (NPD)

although views this plan as an affiliated long-term strategy and as per official announcements in

January 2016, the petroleum investments in Norway (excluding exploration business) will fall to

NK 135 billion in 2016. However, in August 2016, Bente Nyland, head of NPD stated that oil

companies were showing more willingness to complete development plans; as shown by Statoil

which submitted field development plans to the NPD for its Utgard & Byrding oil and gas

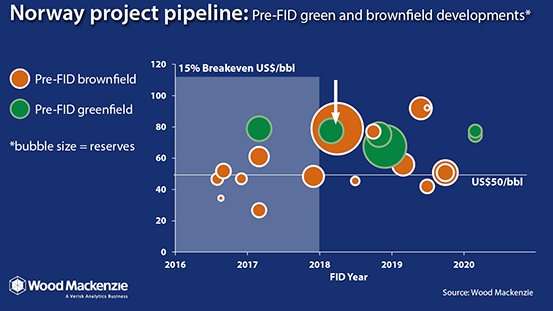

discoveries. High input costs level coupled with low oil prices has posed significant challenges

for oil companies; forcing delayed operational activities and postponed development projects.

But it also brings a positive impact as innovative efforts are seen in existing projects for

achieving operational efficiency and reduction in exploration costs. The forecasted investment

cycle in 2017 also looks bleak with investment value amounting to NOK 150.5 billion as

companies are presumed to be on cost-saving mode; mothballing projects to decommission

aging installations at offshore oil and gas fields. Altogether, the current uncertainties

prevailing in Norway’s petroleum sector are due to contingent factors like reservoirs capability

to deliver, initiating new fields, drilling new development wells and continuity of operational

fields.

The natural gas sector showed more resistance towards depressed global energy markets. The

gas production increased in Norway and gas sales touched 117.2 billion cubic meters in 2015

due to spur in European gas demand. The mode of gas exports to European gas market is

mainly through Norway’s widespread pipeline infrastructure. In the recent wake of Brexit,

Norwegian gas exports to Britain will not get affected; as entrusted by Tord Lien, Norway’s EU

affairs minister. While Norway is not an EU member, but it pays for access to the European gas

market and may just have to negotiate a new trade agreement with London after Brexit. Some

minor gas export to other global customers was also done through LNG option. In terms of

natural gas resources realization, there are two new gas fields scheduled to start production by

the end of 2016 or 2017; namely Martin Linge field in the North Sea holding an estimated 0.7

trillion cubic feet of recoverable gas and the Aasta Hansteen field in the Norwegian Sea holding

approximately 1.6 trillion cubic feet of recoverable natural gas.

From an opportunity perspective, the commencement of Sverdrup gas field project in a declining

oil market conditions has been a boon from project management aspects. It is being developed

with lower input costs and the majority of investments is done in Norwegian currency, which is

putting the project already in profit due to a drop in the value of Norwegian Krone against the US

dollar. Adding to this profit story, the Norwegian suppliers and service providers have proven

cost competitive and Statoil has awarded several contracts to domestic suppliers and EPC

contractors. Overall, the Sverdrup gas field project will prove to be a great lifeline opportunity

for Norway’s petroleum sector.

Norway is also an important LNG (Liquefied Natural Gas) industry player in Europe. In 2014,

Norway delivers 60% of European LNG requirements through its LNG exports. Total LNG

exports from Norway in global gas trade were 5.3 billion cubic meters in 2014. Moreover,

Norway is the forefront runner in fast-growing European small-scale liquefaction industry. It has

three small-scale liquefaction plants through which LNG is distributed by tanker trucks to port

facilities & industrial consumers. The pivotal challenge of small-scale LNG industry is the

absence of proper infrastructure. In short to medium term scenario, the question is as to which

group will commit efforts first to improve the infrastructure. Customers want economic supply

options and suppliers are disinclined to invest in costly infrastructure. Therefore, the need of

the hour is to create investment opportunities in all elements of small-scale LNG value chain.

Summarizing Norway’s role in the global petroleum industry, the Norwegian government

anticipates that the industry will take steps to secure the assets and execute efforts for

minimizing costs; thereby promoting efficiency in all business operations. However, the

government is taking concrete steps to revive the sector by maintaining a steady petroleum

policy. On 29th August 2016, Norwegian Prime Minister Erna Solberg launched the country’s

24th oil licensing round for new exploration areas, majorly off Northern Norway; the focal point

being prospective exploration acreages as a way to maintain the high-value potential of Norwegian

petroleum sector.